The SMILE Curve Has Come for Software

Why software value is migrating to the edges, just like hardware did decades ago

The Middle of the Stack Is Collapsing in Real Time

I recently built a 12-module productivity suite in less than 7 days as a single operator. It was 600,000 lines of code, which a decade ago would have required a well-run software company with 20 engineers and a three-year roadmap.

The interesting question is not how that became possible (more on that later), but what it does to the economics of the middle of the software stack.

Software is following the same arc hardware did.

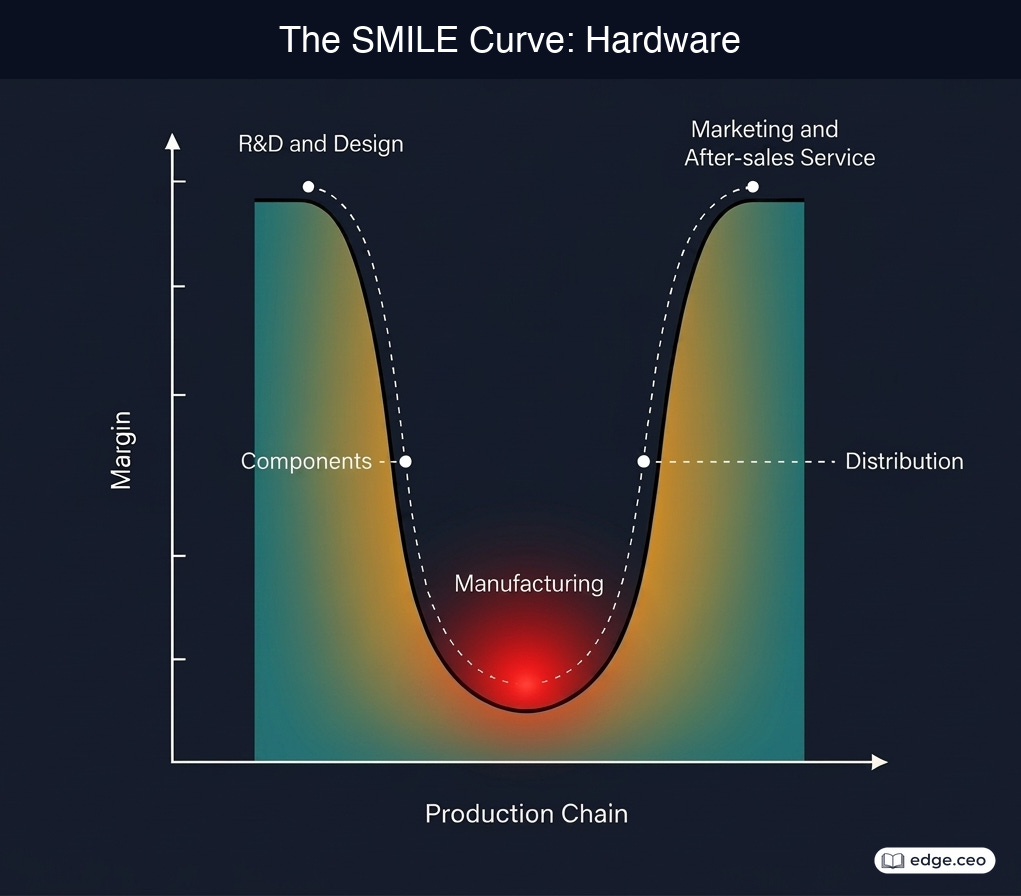

The Curve That Reshaped Hardware

For roughly 30 years, hardware economics followed a stable pattern. Value concentrated at the edges while the middle did the necessary work with far less margin.

Manufacturing economists described this as the SMILE curve, a U-shaped distribution of value across the chain. On the left edge sat R&D and chip design, where companies such as Intel and Qualcomm captured roughly 55-60% gross margins because they owned technical layers that were hard to reproduce. On the right edge sat distribution, brand, and customer ownership, where Apple earned comparable margins by controlling the buying experience, premium positioning, and the direct relationship with the customer.

In the middle sat assembly. Dell, HP, Lenovo, and Foxconn turned components into finished products and moved enormous volume, but they generally operated at 15-20% margins.

That pattern persisted for three decades because the edges owned scarce assets. On one side, deep technical IP and ecosystem control. On the other, demand capture and customer trust.

The Same Curve is Emerging in Software

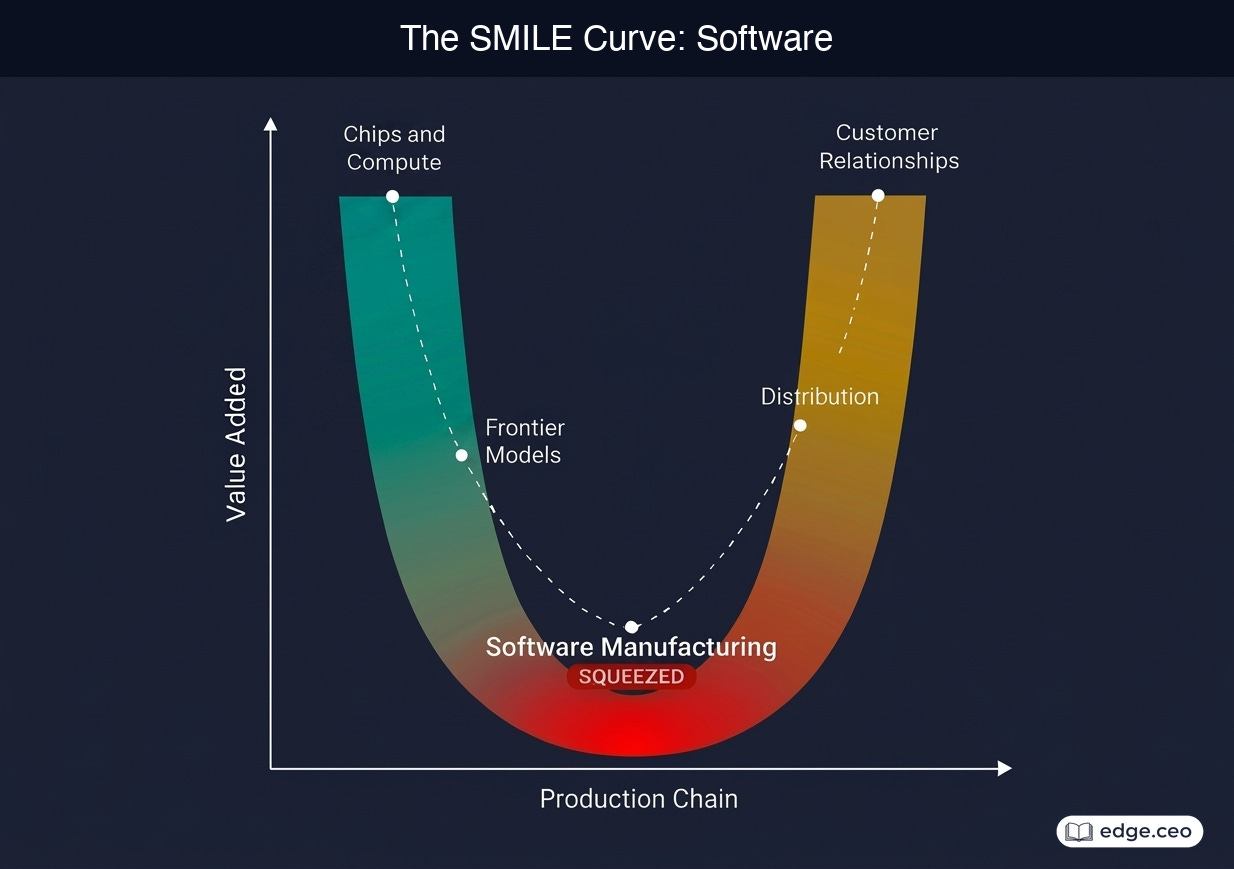

The stack looks different, but the economics are starting to rhyme with hardware: scarce capability on the left, customer control on the right, and a broad middle that is becoming easier to reproduce every quarter. There are five positions in the software value chain, and they do not all compound equally.

The far left is Chips and Compute. Nvidia, TSMC, and AMD design and manufacture the hardware that modern AI runs on, and Nvidia in particular has built a moat that is not just silicon but the CUDA ecosystem wrapped around it. Every new developer building on CUDA deepens the ecosystem and extends the moat. This is the Intel position of the AI era, technically deep and hard to replicate on a 12- to 24-month horizon.

Next is Frontier Models. OpenAI, Anthropic, and Google DeepMind train the foundation models that sit on top of the hardware. Their moats come from training data, research talent, compute scale, and years of iteration. This is distinct from chips: Nvidia does not build frontier models, and frontier labs do not design GPUs. A company with access to unique operational data across billions of interactions has something meaningfully different from one wrapping a generic model around a common interface.

In the center sits Software Manufacturing. This includes SaaS companies building features, CRUD applications, and standard workflows: CRM, project management, helpdesk, internal tools, and back-office systems. SaaS companies sitting here are the Dell and HP of this era, and AI is collapsing the cost of that position toward commodity.

On the right sits Distribution, which includes app stores, marketplaces, channels, partner ecosystems, brand, and any privileged path to customer acquisition. As software becomes easier to build and feature sets converge, the product with the better route to market wins. Buyers in a commodity market choose the name they recognize, the vendor they believe will still exist in 24 months, and the product they feel safe explaining to their procurement team.

At the far right are Customer Relationships. This is where Salesforce and embedded workflow vendors have historically been strongest: deep workflow ownership, retention, switching costs, and customer success. When anyone can build a CRM, the relationship is the product. Workflow depth creates context, context creates embeddedness, and embeddedness creates retention that turns a product into part of the operating system of the customer’s business. This is the Apple position in software, and it is the second edge that can sustain margins near 55-60% even as the middle gets cheaper.

Why the Middle Gets Squeezed First

The middle of the software stack is not disappearing. It is becoming abundant, and abundance changes pricing power long before it removes demand.

A horizontal SaaS product used to justify meaningful valuation premiums by shipping faster than incumbents and wrapping a cleaner UI around familiar workflows. That was defensible when standing up a polished product required a team of 8 to 20 engineers, months of QA, and a material implementation burden. It is much less defensible when AI-assisted development compresses the time to a functional v1 from 6 months to 2 weeks and turns common product patterns into templates. Once the cost of reproducing the middle falls, the middle prices like assembly, and margin migrates toward whatever remains scarce.

That is why so many categories already feel eerily similar, converging on overlapping primitives: records, permissions, workflows, dashboards, notifications, integrations, and AI summaries. The wrapper changes. The economic position does not.

Where to Invest When Building is Free

If the middle is compressing, investment should move to the edges.

The left edge is proprietary technology that compounds with use. The leader’s data, models, and ecosystem deepen faster than any new entrant can assemble their own. The test is simple: can someone replicate the core value in a week? If yes, it is assembly. If no, it is an edge position.

The right edge is customer depth, treated as a primary investment rather than an afterthought once the feature set is complete. As convergence continues, the scarcity shifts from what the product does to how it reaches the buyer and how deeply it embeds in the buyer’s workflow.

The companies that win the next cycle will not be the ones that shipped the most features. They will be the ones that built the deepest positions at the edges while the middle was repricing.

The SMILE curve has come for software.